Strange Tony,

Two of our hospice's new owners, Humana and Welsh, Carson, Anderson and Stowe (WCAS), are longtime bedfellows. Their planned buyout of Kindred is not their first deal.

Current Humana CEO Bruce Broussard worked for U.S. Oncology when it was acquired by WCAS in August 2004. At the time Broussard served as U.S Oncology's Chief Financial Officer.

The

proxy statement listed Broussard as one of a number of continuing investors under WCAS. CFO Broussard

held $3.1 million in U.S. Oncology stock and $4.4 million in options at the time of the buyout. SEC filings indicate Bruce partnered with WCAS by purchasing stock in the private company, .

Bruce

rose to CEO in early 2008 and helped WCAS flip U.S. Oncology in November 2010 when drug giant McKessson bought U.S. Oncology for $2.16 billion. A financial news site reported at the time:

Welsh Carson has unofficially been looking for a buyer for years. The

New York PE firm invested in US Oncology in 2004. “Welsh Carson has

owned it forever,” the banking source says. “It’s well past time they

wanted to sell.”

Welsh Carson also has another health care company up for sale.

Earlier this year, the PE firm put Concentra, which provides health care

and wellness services to employers and the general public, on the

block. Barclays is advising.

The Concentra auction has stalled because there are not a “lot of

logical buyers for it,” the banker says. Concentra is trying to

transform itself from a worker’s health provider to a provider of

primary care clinics, the source says. “The auction is not going well

and they’re trying to sell themselves to another sponsor,” the person

says.

Humana

bought Concentra from WCAS for $790 million in November 2010. A year later Humana

hired Bruce Broussard as CEO. The rationale for hiring Broussard included his experience running physician clinics. He could help Humana integrate and optimize Concentra.

The Concentra deal is echoed by Humana's moves around physician clinics (recently branded

Conviva) and its foray into home health and hospice care with its Kindred and

Curo acquisitions.

Only Humana did not stick with its strategy. It sold Concentra back to WCAS in 2015.

On June 1, 2015, we completed the sale of our wholly owned subsidiary, Concentra Inc., or Concentra, to MJ Acquisition Corporation, a joint venture between Select Medical Holdings Corporation and Welsh, Carson, Anderson & Stowe, a private equity fund, for approximately $1,055 million in cash, excluding approximately $22 million of transaction costs. In connection with the sale, we recognized a pre-tax gain, net of transaction costs, of $270 million which is reported as gain on sale of business in the accompanying consolidated statements of income for the year ended December 31, 2015. The accompanying consolidated statements of income include revenues related to Concentra of $411 million in 2015.

Broussard

said "Concentra’s operations

did not ultimately align with Humana’s

strategy as well as we had originally anticipated." Broussard was hired to make Concentra work but four years later he

flipped Concentra back to WCAS, his former employer.

It’s familiar territory for Welsh Carson, which previously owned both Concentra and Select Medical.

With Humana's financial resources Bruce Broussard could have easily bought Kindred without former employer WCAS or TPG Capital. Including TPG Capital was a nod to the Kindred Board which has TPG director Sharad Mansukani, M.D. as a member. Bruce had this to say

about buying Kindred.

Bruce D. Broussard, Humana’s President and Chief Executive Officer, said, “Humana is focused on enhancing our capabilities for care in the home to prioritize patient wellness while delivering high-quality care in a low-cost setting. This transaction with Kindred underscores the successful and ongoing execution of our strategy by joining with the most geographically diverse home healthcare provider in the country. We are confident that these new capabilities will help Humana continue to modernize home health and meaningfully improve the member and provider experience. We look forward to completing this strategic transaction with TPG and WCAS.”

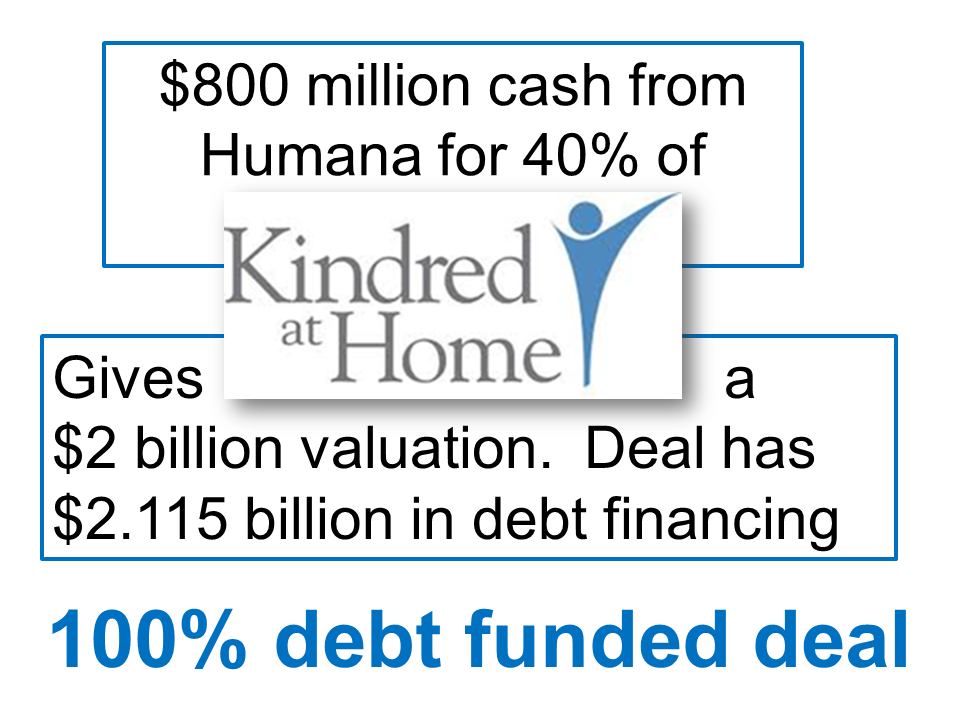

Low cost? Humana and its partners will saddle the home division of Kindred with huge interest expenses by doubling debt for the deal. Kindred borrowed $1.1 billion to buy Gentiva.

Humana/WCAS/TPG will borrow $2.1 billion for virtually the same assets.

Total financing shows over $4.9 billion in

debt/equity to buy Kindred for $4.1 billion. The extra $800 million will likely go toward the Curo transaction and to pay fees/special dividends to Kindred's new owners.

When WCAS bought U.S. Oncology it listed executives and board members who committed to take a stake in the privately held company. The proxy statement read:

Holdings expects that certain executive officers and directors of US Oncology will participate in the merger by making an investment in Holdings and acquiring shares of preferred stock and common stock on the same basis that Welsh Carson and its co-investors are investing in Holdings.

No such disclosure exists for Kindred's sellout to Humana and two financial rapscallions. SEC filings mention employment agreements for David Causby and Ben Breier that may cause conflicts of interest. There is no wording as to how our current board might participate in the deal going forward.

Hospice delivers on Christ's Sermon on the Mount calling and is the strange bedfellow in this greed filled mix. I expect numerous employee violations from CEOs Bruce Broussard and David Causby, the mysterious Curo crew and Humana/WCAS/TPG.

Evidence indicates they prize the earthly over the sacred, the profane over the holy and the diminishing of people over nourishing God's beloved children.

Money-changers will soon buy our hospice and impose their twisted priorities. Lord, help us all.

Anonymous (wanting to serve God's children, not Mammon)